Speak to us now:

1300 728 875

Your adult daughter opens the letter from the super fund six weeks after your funeral. The superannuation balance shows $500,000, but after the tax payable is deducted, she'll actually receive $415,000. That missing $85,000? It went straight to the ATO as superannuation Death Benefits Tax.

This scenario plays out thousands of times each year across Australia. While official death duties were abolished back in 1979, superannuation death benefits are still taxed when they pass to adult children and other non-dependent beneficiaries. The standard rate sits at 17% (15% tax plus 2% Medicare Levy), and can reach up to 32% for untaxed super funds.

With proper planning, you can legitimately minimise this tax burden for your beneficiaries. We will walk you through proven strategies that financial advisors use to protect super benefits from unnecessary taxation, potentially saving your family tens or even hundreds of thousands of dollars.

Let's clear up the terminology first. Australia abolished the death tax back in 1979, so technically, there's no "death tax" anymore. What we're talking about is the Death Benefit Tax: the tax that applies when your super death benefit passes to certain beneficiaries after the member's death.

The tax treatment depends on who receives your superannuation death benefits. If your spouse or financial dependent receives the death benefit, they typically receive it tax-free. But if your adult children receive it and they're not a person financially dependent on you, they'll pay tax on the taxable component of your superannuation balance.

Your super consists of two parts: a tax-free component and a taxable component. The tax-free component always passes to any beneficiary tax-free. The taxable component, however, is taxed at 17% when paid to non-dependent beneficiaries as a lump-sum death benefit. In rare cases involving untaxed elements (mostly public sector super funds), this jumps to 32%.

As an example, let's say you have $500,000 in super, with a typical split of $100,000 tax-free and $400,000 taxable. When your employed 35-year-old son inherits this super lump sum, he pays zero tax on the $100,000 but 17% on the $400,000 taxable portion. That's $68,000 in tax liabilities, leaving him with $432,000 instead of the full amount.

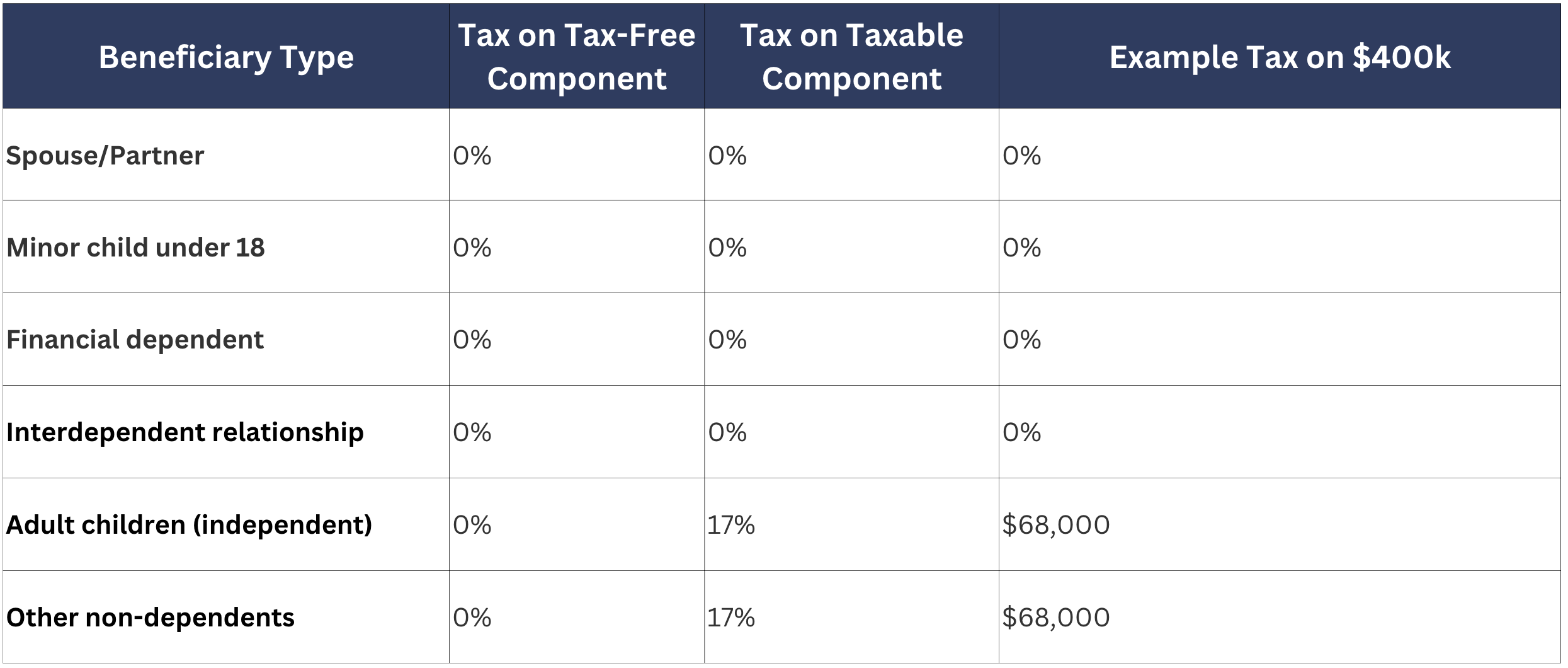

The critical distinction is between dependent beneficiaries and non-dependent beneficiaries under superannuation law. Your spouse, minor child beneficiaries under 18, and anyone who was financially dependent are generally exempt from tax. Your adult children over 18 who are financially independent face the 17% tax burden.

The ATO has a specific definition of "dependent" for death benefit purposes. Dependent beneficiaries include your spouse or de facto partner, children under 18, anyone who was a financial dependent, and people in an interdependent relationship with you.

Interdependency means a close personal relationship where both parties live together and provide financial and domestic support. An adult child caring for a sick parent could qualify as interdependent, as could parents caring for a disabled adult child.

There's also a special exemption: if you inherit super from a deceased police officer or soldier, you're always treated as a tax dependent, meaning the death benefit is received tax-free.

Here's a comparison of tax treatment for different beneficiaries:

It is a common mistake to assume your 25-year-old child who lives independently would be exempt. Unless they were financially dependent on you or you had an interdependent relationship, they'll pay the full 17%.

These are legitimate, ATO-compliant strategies used by financial advisors to reduce your beneficiaries' tax burden.

This is often the most powerful approach for people over 60. You withdraw funds from your superannuation account (tax-free if you're 60 or older), then immediately re-contribute them as non-concessional contributions. This converts your taxable component into a tax-free component.

Let's say you're 62 with $800,000 in your superannuation balance. It's 70% taxable ($560,000) and 30% tax-free ($240,000). You withdraw $120,000 and pay zero tax because you're over 60. You then re-contribute that $120,000. Your taxable component drops to $440,000, and your tax-free component increases to $360,000.

When your adult children eventually inherit these super benefits, they'll save $20,400 in tax (17% of $120,000). You can repeat this re-contribution strategy annually. Over three years, you could convert $360,000 from taxable to tax-free using the bring-forward rule, saving your children $61,200.

The limitation is you're capped at $120,000 per year in non-concessional contributions (2024-25), and you need to be under 75. Starting at age 60 gives you maximum flexibility with this contribution strategy.

A reversionary pension provides a death benefit income stream that automatically continues to your spouse upon your death. This differs from a lump sum payment. The income stream continues tax-free to your spouse, avoiding immediate tax obligations.

However, this only delays the tax issue. When your spouse eventually passes away, and your adult children inherit the remaining superannuation assets, they'll still face 17% tax on the taxable element. You need to combine this with other strategies that address what happens at the member's death of the second spouse.

The immediate benefit is clear, though. Instead of paying tax on a lump sum death benefit, it continues as a super income stream to your spouse, completely tax-free.

This might sound obvious, but it's overlooked. If you're over 60 in the retirement phase, you pay zero tax on pension withdrawals. Your children will pay 17% tax on the amount they inherit as superannuation death benefits. The math is simple: you spend it, you save more.

Many retirees leave large superannuation balances that get heavily taxed. If you have $900,000 and withdraw an extra $30,000 per year for 10 years, that's $300,000 in tax-free withdrawals. Your children saved $51,000 (17% of $300,000) that would have been tax payable on the deceased person's super.

The key is working with a financial advisor to model your financial situation and longevity. Once confident you have enough, spending down your total superannuation balance becomes tax-effective.

If you and your spouse have unequal superannuation balances, consider equalising them. The higher-balance spouse can withdraw funds and recontribute to the lower-balance spouse's super. This spreads your entire member balance across two people.

For example, the husband has $1.2 million, and the wife has $400,000. Upon the husband's death, $1.2 million passes to his wife tax-free. But when she eventually dies, their adult children face a much larger tax bill on the combined balance.

Instead, the husband withdraws over several years and makes non-concessional contributions to his wife's super. Now they each have roughly $800,000. When the survivor dies, the children inherit a smaller taxable amount, meaning less tax.

This works best when started early, ideally in your 60s, because it takes several years to move large amounts within contribution limits.

A binding death benefit nomination is a legal instruction to your super fund trustee about who receives your super benefits. Unlike non-binding nominations, which give the trustee discretion, a binding nomination must be followed.

From a tax perspective, you can strategically direct super. You might nominate your spouse for the bulk (received tax-free), and smaller amounts to your member's estate for distribution through your will as the legal personal representative directs.

The most important thing is to keep them up to date. Many expire after three years, and outdated nominations are costly mistakes. If yours still lists your ex-spouse or doesn't reflect your current family, it needs to be updated immediately.

This strategy doesn't reduce the tax rate, but it offsets the impact. You hold life insurance within your super fund, sized to cover the anticipated tax burden.

For example, you have $500,000 in super and take out $100,000 in life insurance inside your super fund. When you die, the total death benefit is $600,000. After 17% tax (roughly $102,000), your children receive about $498,000, close to your original balance.

The trade-off is that insurance premiums reduce your superannuation balance over time. You need to weigh annual premium costs against the certainty of offsetting the tax burden.

This works best for modest balances ($300,000 to $800,000) where premiums are affordable.

You can withdraw super and use it to balance your non-super assets. When your children inherit property or shares outside super, they pay no tax on inheritance itself. CGT only applies when they later sell the asset, with a 50% discount if held over 12 months. This is often more tax-effective than inheriting super, which faces immediate tax.

By using your super to fund a lifestyle in retirement and preserving non-super assets for inheritance, you shift wealth into a more tax-effective form for your beneficiaries.

Even with good intentions, small errors can cost your family tens of thousands.

No valid binding death benefit nomination is the biggest problem. If your super fund doesn't have current instructions, your super may go to the deceased's estate by default, pass through probate, and cause delays. Review your nominations every 2 to 3 years and after major life events, such as marriage or divorce.

Keeping super in the accumulation phase after retirement is another missed opportunity. Once you're 60 and retired, you should strongly consider entering the retirement phase and implementing the recontribution strategy. Every year you delay is a lost chance to convert $120,000 from taxable to tax-free.

Assuming you will control your super is dangerous. Superannuation operates independently unless your binding death benefit nomination directs it explicitly to your deceased estate, where the legal personal representative distributes it according to your will.

Not reviewing after major life events creates problems. Marriage, divorce, birth of children, or changes in a child's dependency status all require reviewing your super death benefit nominations and overall strategy.

If your superannuation balance is over $500,000, professional advice isn't optional. A comprehensive strategy might cost $2,000 to $5,000, but could save your beneficiaries $50,000 to $300,000 or more.

You definitely need to seek advice if you have a blended family, own an SMSF, have disabled or financially dependent adult children, or haven't reviewed your strategy in five years or more.

The right time to act is now, especially if you're between 60 and 70. This is your optimal window. You have maximum flexibility; all strategies are available, and you have enough years to implement multi-year plans like the re-contribution strategy.

A financial advisor can help you understand your tax-free component versus taxable component split, model different scenarios for your financial situation, ensure your binding death benefit nominations are valid, coordinate with your legal personal representative and estate planning, and implement strategies that align with your personal objectives.

Superannuation death tax is significant, but it's not inevitable. The seven strategies outlined here are used every day by financial advisors to help Australian families protect super benefits from unnecessary taxation. Some are simple, like updating your binding death benefit nomination. Others require years of planning, such as systematic re-contribution or spouse equalisation.

The cost of doing nothing is real. Without planning, your adult children could lose $50,000, $100,000, or even $300,000 to tax obligations that could have been minimised. You worked decades to build that superannuation balance. With the right planning, more of it can go where you intended.

Start by finding your latest super statement and checking the split between your tax-free and taxable components. Then check when you last updated your binding death benefit nomination. Those two actions alone will tell you whether you have an urgent issue.

If you're looking at these strategies and feeling overwhelmed about where to start, that's completely normal. Superannuation Death Benefits Tax planning involves technical requirements, contribution caps, and coordination between your super fund, estate planning, and tax obligations.

At Darcy Bookkeeping & Business Services, we work with clients across Australia to develop practical superannuation strategies that protect their families from unnecessary tax. We can help you understand your current position, identify which strategies suit your financial situation, and implement them properly. If you'd like to discuss your super death benefit planning, get in touch with us.

"*" indicates required fields